👋 Bhupendra Rawat

Stock Market Data Analyst | Programming Enthusiast | 4+ Years of Experience

Empowering insights with data & code🔍 Expertise:

- Fundamental & Technical Analysis

- Python & Pandas for Stock Data

- Interactive Financial Dashboards

- JavaScript & Chart.js Visualization

🔄 Last Updated: Analysis Based on Data Till 3 August 2025

🚗 Tata Motors Share Price Target 2030/2025: Reclaiming Momentum in the Auto and EV Race?

Tata Motors Ltd, a leader in India’s automotive sector, operates across passenger vehicles, commercial vehicles, and electric mobility through its Tata EV and Jaguar Land Rover (JLR) divisions.

The share price outlook for Tata Motors by 2025–26 will likely be shaped by:

📈 Sustained demand in the EV segment and domestic passenger vehicles

📊 Growth in JLR global sales and premium SUV markets

💰 Margin recovery supported by operating leverage and cost controls

🔋 Expansion in EV infrastructure and product launches in India

🌍 Export performance and geopolitical stability in key overseas markets

With growing traction in electric vehicles, improving financial metrics, and a strong brand portfolio, Tata Motors is poised for long-term upside. However, risks like raw material inflation, chip shortages, and global economic slowdown could impact near-term sentiment.

Still, Tata Motors’ transformation story—from losses to profitability—backed by innovation and strategic vision, makes it a high-potential auto stock in India’s evolving mobility space.

✅ Tata Motors Target View – 2025, 2026 & 2030

If global headwinds persist, raw material inflation continues, or JLR underperforms, Tata Motors’ stock could fall to ₹600 in the near term.

However, if EV adoption rises, JLR margins expand, and India’s auto demand remains strong, the stock could reach ₹1,200+ by 2026 and ₹2,000+ by 2030.

📉 Downside Risk 2025: ₹600 (approx. -16.7% from ₹720 base)

📈 Upside Potential 2026: ₹1,200+ (approx. +66%)

📈 Upside Potential 2030: ₹2,000+ (approx. +178%)

🔎 Note:

These targets are not guaranteed and depend on Tata Motors’ execution in EV leadership, JLR’s performance, macroeconomic trends, and margin stability. Long-term investors should monitor earnings consistency, ROE, and global market share growth.

📊 For Short-Term / Intraday Traders:

If you want daily trading levels, live analysis, and intraday strategies for Tata Motors and other stocks —

join our free Telegram group, where you get professional-level market insights and trading guidance every day.

📊 Tata Motors Financial Overview (2021–2025)

📊Tata Motors Fundamental Analysis: Evaluating the Core Strength of the Company

This section examines key financial metrics like revenue, net profit, EPS, ROE, and debt-to-equity ratio to understand Tata Motors’ growth trajectory and long-term potential.

🔸 Revenue & Growth

Tata Motors has shown a strong revenue rebound since FY21, especially post-COVID, with a CAGR of 15.18% between FY21 and FY25.

| Year | Revenue (₹ Cr) | Revenue Growth (%) |

|---|---|---|

| 2021 | 2,49,794.75 | – |

| 2022 | 2,78,453.62 | 11.47% |

| 2023 | 3,45,966.96 | 24.25% |

| 2024 | 4,37,927.77 | 26.58% |

| 2025 | 4,39,695.00 | 0.40% |

📈 Revenue peaked in FY24 and remained steady in FY25, reflecting stabilization after a strong recovery phase.

🔸 Net Profit & Margins

After reporting losses in FY21 and FY22, Tata Motors turned profitable in FY23. Margins have significantly improved as the company gained operational efficiency.

| Year | Net Profit (₹ Cr) | Net Profit Margin (%) |

|---|---|---|

| 2021 | -13,016.14 | -5.21% |

| 2022 | -11,234.70 | -4.03% |

| 2023 | 2,353.49 | 0.68% |

| 2024 | 31,106.95 | 7.10% |

| 2025 | 27,862.00 | 6.34% |

💡 Net margins turned positive in FY23 and are now above 6%, a promising sign of Tata Motors’ turnaround.

🔸 EPS & Growth

Earnings per share (EPS) followed a similar trend as net profit — sharp recovery after losses.

| Year | EPS (₹) | EPS Growth (%) |

|---|---|---|

| 2021 | -37 | – |

| 2022 | -30 | -18.92% |

| 2023 | 6 | -120.00% |

| 2024 | 82 | 1,266.67% |

| 2025 | 79 | -3.66% |

📊 EPS jumped dramatically in FY24, indicating a strong earnings recovery. Slight dip in FY25 reflects margin normalization.

🔸 Return on Equity (ROE)

ROE shows how efficiently Tata Motors is utilizing its equity to generate profits. The company has made a remarkable comeback in this metric.

| Year | Net Profit (₹ Cr) | Average Equity (₹ Cr) | ROE (%) |

|---|---|---|---|

| 2021 | -13,016.14 | – | – |

| 2022 | -11,234.70 | 49,900.78 | -22.51% |

| 2023 | 2,353.49 | 46,187.09 | 5.10% |

| 2024 | 31,106.95 | 67,641.76 | 45.99% |

| 2025 | 27,862.00 | 1,03,035.60 | 27.04% |

📈 ROE surged past 45% in FY24 — an exceptional figure. Even at 27% in FY25, it reflects strong capital efficiency.

🔸 Debt-to-Equity Ratio

Despite high debt levels, Tata Motors has steadily improved its debt profile over time.

| Year | Total Debt (₹ Cr) | Debt-to-Equity |

|---|---|---|

| 2021 | 2,86,305.59 | 5.18 |

| 2022 | 2,81,787.63 | 6.32 |

| 2023 | 2,80,981.87 | 5.88 |

| 2024 | 2,75,022.13 | 3.14 |

| 2025 | 2,53,424.00 | 2.14 |

📉 Debt-to-equity has improved significantly from over 6x to just above 2x — a major positive for long-term financial health.

🔸 Cash Flow Overview

Cash flows highlight the company’s operational strength and capital allocation. FY24 and FY25 saw strong cash from operations, despite high investing and financing outflows.

| Year | Operating CF (₹ Cr) | Investing CF (₹ Cr) | Financing CF (₹ Cr) | Closing Cash (₹ Cr) |

|---|---|---|---|---|

| 2021 | 29,000.51 | -26,126.25 | 9,904.20 | 31,700.01 |

| 2022 | 14,282.83 | -4,775.12 | -3,380.17 | 38,159.01 |

| 2023 | 35,388.01 | -16,804.16 | -26,242.90 | 31,886.95 |

| 2024 | 67,915.36 | -22,828.09 | -37,005.99 | 40,014.76 |

| 2025 | 63,102.00 | -47,594.00 | -18,786.00 | 34,349.00 |

📌 Positive operating cash flows in FY24 and FY25 show strong core business generation. Rising investing cash outflows may be linked to EV and tech expansion.

✅ Conclusion

Tata Motors has shown a remarkable financial turnaround, driven by:

🚗 Strong revenue growth post-pandemic

💰 Return to profitability and improved margins

📈 High ROE reflecting capital efficiency

📉 Reduced debt levels and improving debt-equity ratio

🔋 Increased cash generation despite high investments

🔎 Investor View:

With EV adoption, global demand recovery, and better cost control, Tata Motors appears well-positioned for sustainable growth toward 2030. Its fundamentals support the long-term investor narrative.

📈Tata Motors Technical Analysis: Price Charts, Trends & Potential Movements

Here, we analyze price action, support/resistance levels, moving averages, RSI, MACD, and other indicators to forecast near- and long-term movements.

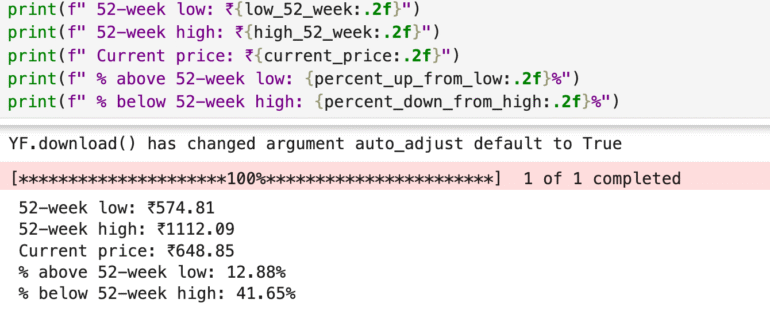

📈 Tata Motors Share Performance Snapshot (2025)

🔻 52-week Low: ₹574.81

🔺 52-week High: ₹1112.09

📊 Current Price: ₹648.85

➡️ Above 52-week Low by: +12.88%

⬅️ Below 52-week High by: -41.65%

📌 Tata Motors is trading nearly 13% above its 52-week low, showing early signs of recovery. However, it’s still over 40% below its peak, indicating room for further upside. If EV momentum, export growth, and cost controls continue, the stock could regain strength toward previous highs.

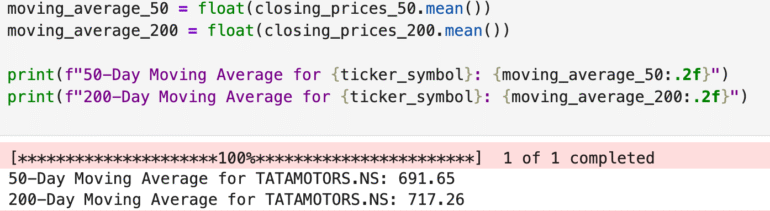

📉 Tata Motors Technical Overview (2025)

📊 Current Price: ₹648.85

📈 50-Day Moving Average (DMA): ₹691.65

📉 200-Day Moving Average (DMA): ₹717.26

🔍 Analysis:

Tata Motors is currently trading below both its 50-DMA and 200-DMA, indicating short-term and long-term weakness or investor caution.

While this may reflect profit booking or sectoral consolidation, it could also signal a potential buying opportunity if the fundamentals remain intact and broader market sentiment improves.

📌 Conclusion:

The stock’s position below key moving averages suggests bearish pressure, but long-term investors may watch for signs of reversal or accumulation, especially if future growth triggers (like EV expansion or export demand) start playing out.

🔍 Competitor Analysis: Tata Motors EV

Tata Motors EV, India’s largest electric vehicle manufacturer, offers a diversified portfolio of passenger and commercial EVs. With a strong brand, extensive distribution network, and government-backed incentives, it leads the EV market.

Key Competitors:

✅ This analysis highlights Tata Motors’ leadership, while Wardwizard, Bajaj Auto, and Mahindra Electric provide competitive pressure in different EV segments.